2017 marked the first solar eclipse in the United States since 1979, perhaps a fitting spectacle given the stark contrast of light and dark moods that collided in our nation last year. On the one hand, optimism is at record levels – consumer confidence reached 17-year highs, business optimism is the highest on record, and the VIX (Volatility Index – aka the “Fear Index”) indicates investors are as sanguine as they’ve ever been. On the other hand, pessimism is also at record levels – the Hedonometer (Twitter’s Happiness Index) fell to an all-time low following October’s Las Vegas massacre, our President’s approval ratings reached record lows in December, and geopolitical tensions are the worst we’ve seen in decades.

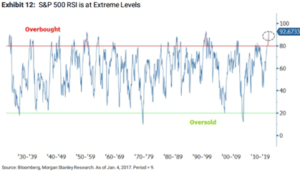

Nonetheless, as rare as solar eclipses come, an even more unlikely event occurred in the financial markets last year. It is true the S&P exceeded 20% for only the 6th time in the last 20 years, but what was most unusual about 2017 was the index did not experience a single down month. Remarkably, that is the first time that has happened in a dataset stretching back 90 years!

A number of very good things happened that made 2017 a special year for the markets:

Strong Corporate Earnings

According to FactSet, S&P earnings last year likely grew 9.6% (best since 2011) and every one of the 11 major S&P 500 sectors experienced positive growth. That trend is expected to continue into 2018 with revenues estimated to grow 5.6% and earnings estimated to expand another 11.8%.

{kind=link}