Normal is an illusion.

Morticia Addams

What is normal for the spider is chaos for the fly.

Changes in the Patterns

The concept of normality is not rooted in fundamental truth; it is merely the perception of what condition or behavior would be considered typical or expected based on historical patterns. Humans are attracted to patterns; our brains are hardwired to recognize patterns to guide us in making judgments, make decisions, and acquire knowledge. A break in the pattern makes us uncomfortable. In fact, the very definition of “chaos,” according to Merriam-Webster, is “complete confusion and disorder.” One year ago, the world experienced a significant break in the pattern in the form of a pandemic that dramatically altered the way we live, igniting a ripple effect causing breaks in other patterns in our lives and setting off a chain of potentially new patterns. These possible new patterns are often more colloquially referred to as “the new normal.”

There’s been tremendous interest in what “the new normal” may look like. Google saw a massive spike for the term “new normal” in web searches last year. With around 100 million Americans now either partially or fully vaccinated, many cities and states have accelerated their efforts to reopen businesses, schools, churches, and events leaving many of us to wonder what parts of our day-to-day lives in the future may resemble the old “normal” and what parts may be permanently changed.

Similar questions are permeating throughout the social fabric. Questions have been raised about our politics, our prejudices, our priorities, and indeed, our very culture. Investors and economists are contemplating a “new normal” of record debt, historically low rates, unprecedented fiscal and monetary stimulus, and potential tax increases to fund an ambitious infrastructure bill. Can such factors be sustainably and steadily maintained or does this mark the beginnings of a more dangerous pattern for the future?

A Difference of Opinion

Perhaps the biggest question that lies at the heart of many investors’ concerns is reflected in the price action that has been occurring in interest rates. Since the start of the year, the key 10-year US Treasury yield has flown higher, going from 0.93% at the beginning of January to 1.72% in just three short months.

While the pace of the move has been surprising to many, what is particularly remarkable is that it has occurred in the face of ongoing rhetoric from Fed officials that the central bank intends to keep rates low for the foreseeable future. In January, Fed Chairman, Jay Powell, said that the time to raise interest rates to address inflation “is no time soon” and in February reiterated that policy would remain “patiently accommodative” as the employment picture still has a “long way to go.”

Given the magnitude of the rates selloff, however, it is clear the market has taken a very different perspective. For example, In early March, Chairman Powell expressed skepticism that inflation could sustainably rise above 2%, but a consumer survey the following week showed that average Americans expect their 12-month inflation rate to be 3.1%. Furthermore, last week the Financial Times published an article entitled, “US companies sound inflation alarm,” highlighting scores of companies adding their voices to the growing chorus of concern about the potential pace of inflation.

Should inflation actually reach such levels and beyond, this could serve as a significant end to a several years’ long era of low interest rates and low inflation. By comparison, unfortunately households are currently less optimistic about their income growth, estimating just a 2.4% increase over the next 12 months. While a combination of higher price inflation and lower wage inflation would certainly be troubling, over the last decade the market has expressed concerns about inflation in 2011, 2014, and 2018; only to see inflation fall short each time. Chairman Powell has acknowledged that while he expects inflation to rise as the economy recovers, he expects the gains to be just temporary. Former Pimco CEO, Mohamed El-Erian, has echoed similar sentiments. He believes that rather than seeing significant sustained inflation, more likely we will see a short-term “price pop” as the economy first reopens and demand far outstrips supply before eventually finding greater equilibrium.

Stocks Continue the Upward Trajectory Despite Higher Rates

Rising inflation expectations have also affected moves in the stock market. As longer-term rates have moved higher, investors are discounting future earnings and therefore shifting away from growth stocks (which derive the bulk of their worth from future growth) toward value stocks (whose worth is more driven by current earnings). The two best performing sectors so far this year have been energy (+32.7%) and financials (+16.8%), which also happened to be the two worst performing sectors of 2020; thereby undoing at least some of the damage from last year.

Moreover, this combination of higher rates and higher stocks has also resulted in a widening gap in equity vs fixed income performance. The S&P 500 rose 5.77% in the first quarter while the Barclays AGG fell -3.69% over the same period. With the stock market’s performance thus far this year, plus a 16% gain in 2020 and a 29% gain in 2019, recent valuations (around 22x forward P/E) have become stretched to levels not seen since early 2001. So, the question remains, with rates having virtually retraced themselves back to nearly pre-pandemic levels, why haven’t earnings multiples come down yet?

Various Supportive Factors

Corporate earnings expected to move higher

According to FactSet, by the end of the first quarter, 60 S&P 500 companies have issued positive earnings guidance. This is the highest number of companies to have issued positive earnings guidance since FactSet began tracking the measure in 2006, breaking the current record of 57; which just occurred last quarter (Q4 2020). The data is further reinforced by the fact that 69 S&P 500 companies have issued positive revenue guidance by the end of the first quarter, which would also be a record. This suggests that the earnings increases are being driven by stronger revenues rather than reduced expenses, which is a welcome sight for investors.

Economic forecasts are also improving

It isn’t just corporate earnings being adjusted higher; economists are also raising their GDP estimates for 2021. According to FactSet, the average growth expectation among analysts for 2021 is 4.7%, which is considerably higher than the 3.9% that was estimated at the end of November. More recently, though, some forecasters are becoming significantly more bullish. In mid-March the Federal Reserve increased its growth estimate to 6.5% for 2021 (up from 4.2% in December) and Goldman Sachs raised its growth target for the year to 8%; which if achieved would be the fastest pace of growth since 1951. The Wall Street firm is similarly bullish on jobs growth – forecasting that US unemployment will fall to just 4% by the end of the year, 3.5% in 2022, and 3.2% in 2023. If the recent jobs report is any indication, last month’s nonfarm payrolls rose by 916,000 in March, far ahead of the consensus estimate of 675,000 and upward revisions were also made to the job additions in January and February. Harvard Professor and Senior Fellow at the Peter Institute for International Economics, Jason Furman, found that if jobs growth continues at this current rate (an admittedly big “if”), it would take until May 2022 to be at a point for the US as though the pandemic had never occurred at all.

Additional stimulus to stoke the flames

After spending $3.5 trillion on COVID-related stimulus last year, the government passed another $1.9 trillion in the American Rescue Plan on March 11. This bill includes direct payments to individuals, aid to state and local governments, the extension of unemployment benefits, tax incentives, health funding, education, and other programs. Some economists anticipate that the stimulus plan, which has the potential to turbocharge the US economy, may even result in US economic growth outpacing that of China in 2021 for the first time in 45 years, according to Fortune.

Not out of the woods yet, though

The American Jobs Plan

While the recent stimulus rescue was passed relatively smoothly, President Joe Biden’s ambitious $2+ trillion infrastructure bill will be a more complicated undertaking. There has been plenty of debate amongst politicians about the definition of “infrastructure.” The bill is expected to face plenty of resistance from Republicans and may see several different iterations in the coming months. The current proposed legislation is to increase the corporate tax rate from 21% to 28% in order to fund the new spending over 15 years.

The Curve is Steepening Again

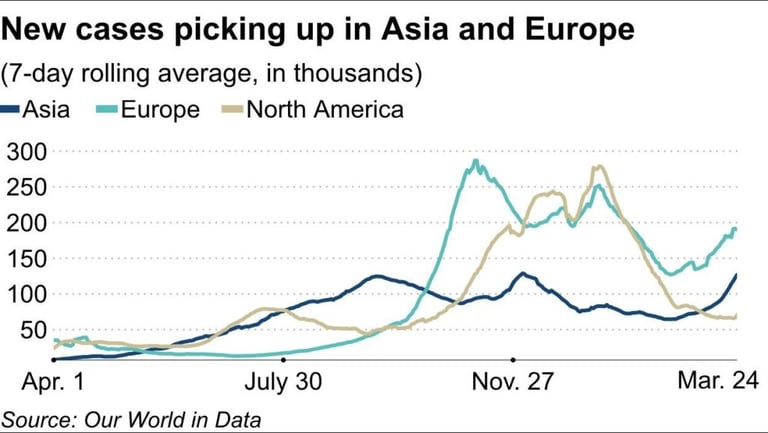

Although approximately 100 million Americans have now been at least partially vaccinated, new COVID case numbers have been trending higher across the world, including the United States. According to Axios, the US has reported 63,000 daily new cases over the past week, a 17% increase from the week before. In fact, in the last week of March, only seven states reported declining new cases. The majority of states are instead reporting higher case numbers. Increasingly, experts are warning that achieving herd immunity to SARS-CoV-2 may be an impossibility, with a more likely scenario being coexistence similar to the influenza. Across the Atlantic, cases have been surging in Europe. The region is coping with a third wave and countries such as France, Italy, and Poland have been forced once again go on lockdown. New cases are also rampant in South America and are spiking once again in Asia.

One Familiar Pattern

Looking back more than one year since the world was stunned by the pandemic, what started as a scientific and medical problem remains just that: a scientific and medical problem. With jobs racing back, consumers spending healthily again, companies operating at a high level, and a stock market that just broke above 4000 for the first time, the economy’s ability to recover is not the significant concern it was 12 months ago. That said, however, if we are unable to successfully manage the infections and spread of the disease, everything else becomes moot. Any hope of a return to the old “normal,” or a shift towards an optimistic “new normal,” is dependent on overcoming the virus.

This Easter season, we celebrated a holiday that commemorates the restoration of life. That the world finds itself engaging in this very effort at this particular time is a fascinating synchronicity.