At the heart of the Uniform Prudent Investor Act and the principles of risk, return, and diversification is Modern Portfolio Theory (MPT). This theory was introduced by Harry Markowitz in two seminal papers written 1952 and 1959, and his pioneering work later won him the 1990 Nobel Prize in Economics.

Risk and Return

Markowitz proposed that there was a relationship between risk and return - investors are willing to take on greater risk when there is potential for greater return. In other words, even though there might be essentially risk-free assets, e.g. US Treasuries, investors are willing to invest in riskier assets in order to obtain a return that meets their investment objective.

Markowitz wanted to know if it was possible to construct a portfolio based on an investor’s required return while reducing the portfolio’s overall potential risk of loss. He was able to show mathematically that there was a way to combine assets together in a portfolio while actually decreasing the portfolio’s risk. The key to reducing risk was through diversification.

Correlation

But how does a trustee know if a portfolio’s underlying assets are diversified? Or how does one create a portfolio that is properly diversified? Markowitz, in his papers, explained that there was a simple way to determine this using a mathematical concept called correlation.

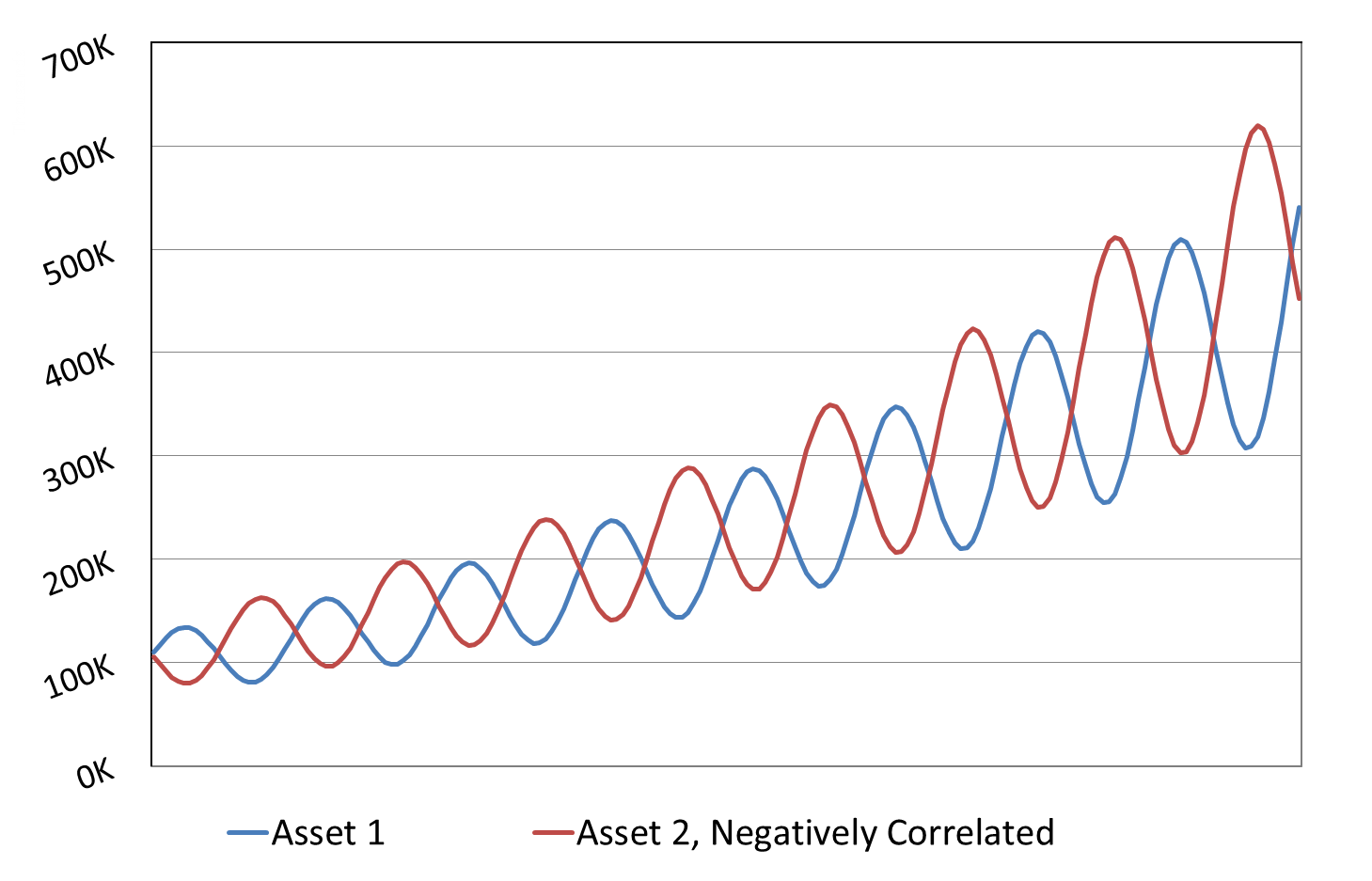

Correlation represents a relationship between the returns of two or more investments. If these investments both go up or down in value at the same time, then the investments are said to be positively correlated.

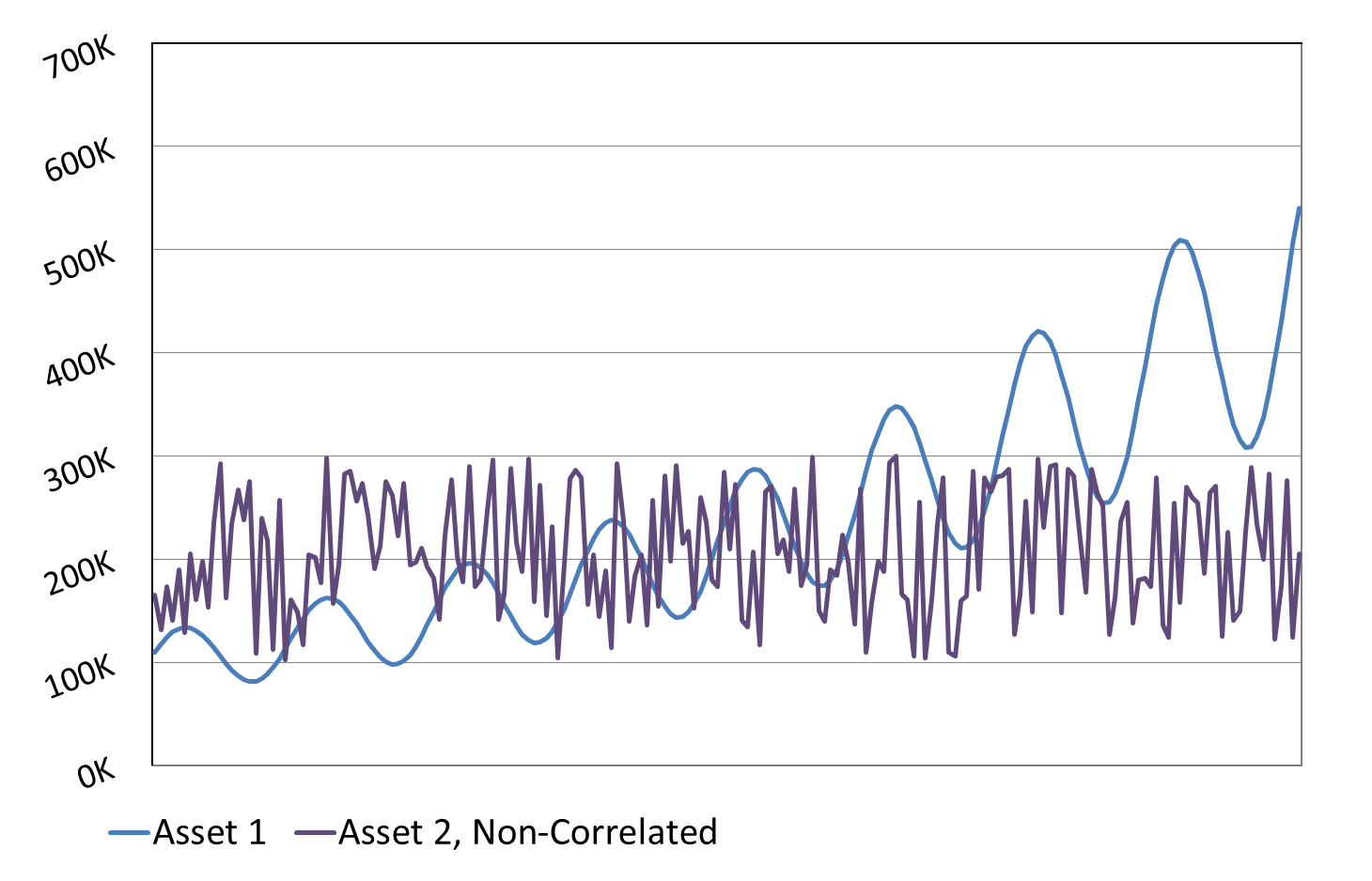

Finally, if the investments are not related in their movements, then the investments are considered non-correlated.

Correlation is an important part of Modern Portfolio Theory because it provides a measurable way to determine whether individual portfolio assets are related to each other. In Modern Portfolio Theory, this measurement used in conjunction with measurements of risk and return can help find a more efficient portfolio than one that is not diversified.

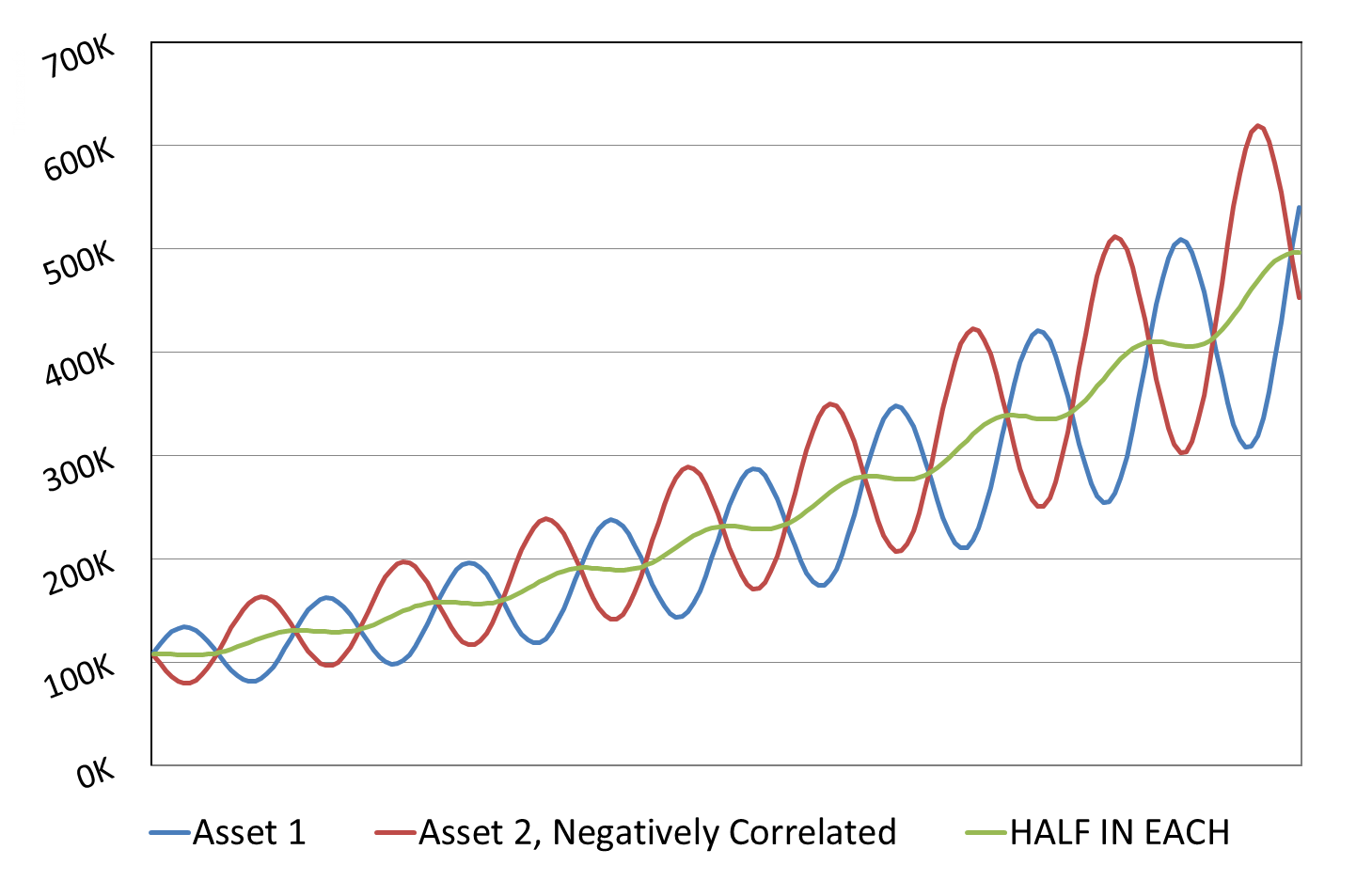

To use a simple example, if two assets are negatively correlated and combined together into a portfolio, the result would be a portfolio with less volatility. The below scenario is purely hypothetical, but it shows the impact that understanding correlation can have on portfolio construction.

If correlation is not part of the portfolio creation process, then the portfolio itself might end up being exposed to more risk than necessary. A portfolio might seem to generate a good return while taking on less risk, but when the underlying securities are highly correlated the portfolio will actually have higher risk and a higher potential for loss.

This is why Uniform Prudent Investor Act statute state that:

(b) A trustee's investment and management decisions respecting individual assets must be evaluated not in isolation but in the context of the trust portfolio as a whole and as a part of an overall investment strategy having risk and return objectives reasonably suited to the trust.

To manage a portfolio in the client’s best interest, a trustee should consider the portfolio’s risk and return objectives. And in order to know if a portfolio is taking on more risk than necessary, a trustee can use correlation to determine whether the portfolio is properly diversified.

To manage a portfolio in the client’s best interest, a trustee should consider the portfolio’s risk and return objectives. And in order to know if a portfolio is taking on more risk than necessary, a trustee can use correlation to determine whether the portfolio is properly diversified.

It is important for trustees to understand the general concepts of Modern Portfolio Theory, such as risk, return, and diversification. If trustees are unfamiliar with these principles and seek to invest according to a strategy of investments with the highest potential for return, they may unknowingly create a portfolio that is not appropriately diversified or that has a high amount of risk.

Taxation

Expected tax consequences of investment decisions or strategies (c)(3).

Trusts can be taxed differently depending on the purposes and provisions. For example, revocable trusts are usually set up to benefit the grantor (the person funding the trust) and as a result, gains and distributions are passed through to the beneficiary’s income tax bracket. On the other hand, irrevocable trusts are taxed by the IRS at the trust level and not at the individual tax bracket level.

A trustee who is less familiar with trust taxation might find the UPIA statute daunting because of the interplay between taxes, income, and total return. For example, there are situations when the selling of specific assets within a trust, in order to help bring the trust in compliance with the diversification mandate, could result in large capital gains. If a trustee is managing an irrevocable trust, the impact of realized capital gains is even greater because of the trust’s compressed tax bracket.

A trustee should work with both the CPA and the investment advisor to develop an appropriate plan for the investments. Aside from realizing gains, there are other potential tax considerations that might apply to the trust: principal versus income assignment with regards to mutual fund short-term and long-term capital gain dividend distributions, step up in basis, or retaining eligibility for government benefits. This is where having both a qualified advisor and CPA can be extremely beneficial.

Liquidity

Needs for liquidity, regularity of income, and preservation or appreciation of capital (c)(7).

When supervising or managing investments, a trustee also needs to consider whether investments are sufficiently liquid. Investments that are less liquid are often more risky, but may also have a greater chance of appreciation. On the flip side, they can also be challenging to transact in and out of.

If a trust requires a regular distribution of income, then certain investments might not be appropriate if they are not liquid. This is why a trustee should understand the definition of liquidity and how it relates to the trust’s investments. Liquidity refers to the speed at which an asset can be converted to cash without impacting the investment’s market price.

Liquidity Example: An annuity is an example of a popular investment that is easily convertible to cash. However, annuities that have surrender charges (5 to 7 year periods is not uncommon) would not be considered liquid. This is because selling the annuity back to the insurance company results in a large surrender penalty charge of up to 10%. This surrender charge in turn affects the proceeds from the sale. So although investing in an annuity could provide a regular source of income, the annuity itself might be inappropriate for a trust if the trust allows for large distributions to occur outside the normal annuity schedule.

One of the critical changes the UPIA made to the 1959 rule was the authority to delegate. Section 9 of the code allows for delegation, but charges the trustee to exercise care, skill, and caution when:

- Selecting an agent

- Establishing the scope and terms of the delegation in relation to the trust

- Monitoring and reviewing the agent’s performance and compliance

Trustees do not have to delegate their investment decision making. However, if they do not have the knowledge or experience to make investment decisions according to the standards provided by the UPIA, it is recommended that they delegate this responsibility to an investment advisor who does have that expertise.

According to the UPIA, trustees who properly delegate their investment authority and appropriately monitor are not held liable for the decisions made by the investment advisor.

Selecting an Agent

When selecting an advisor, trustees need to show that they have done appropriate due diligence. This can include using websites such as FINRA or the SEC to verify licensing, disclosures, and/or complaints.

A trustee should also understand the differences between suitability and fiduciary standards. Financial professionals who follow the suitability standard are duty-bound to provide investment advice suitable for the situation, but are not obligated to act in the client’s best interest. Investment advisers who follow the fiduciary standard are required to put the client’s best interest first. One of the reasons why a trustee should understand these differences is to make sure the financial professional’s methods align with the trustee’s.

Compensation

Financial professionals who follow a suitability standard are more likely to be compensated on a commission basis, while those who follow a fiduciary standard are more likely to be compensated on an ongoing fee basis. However, UPIA compliance for a trust portfolio is not a one-time event; the stock market, economic conditions, and political environments are constantly changing. Trustees generally use investment advisors who follow the fiduciary standard because they are compensated on an ongoing basis for their advice. The adviser is obligated to put the trustee’s best interests first, which aligns with the trustee’s own legal requirements of fiduciary duty.

Finally, there are also representatives who are dually licensed, which means they operate under both the suitability and fiduciary standard. If the trustee chooses to work with a dually licensed individual, they should have clear written agreements as to which standard is being adhered to.

Managing Costs

Another aspect of selecting an agent is the trustee’s duty to manage costs. Section 7 of the UPIA states:

“In investing and managing trust assets, a trustee may only incur costs that are appropriate and reasonable in relation to the assets, the purposes of the trust, and the skills of the trustee.”

When selecting an agent, the trustee should consider the various costs that may be incurred because of the investment professional’s management. These may include commissions, underlying mutual fund or ETF expense ratios, adviser management fees, trading expenses, and even additional trust accounting costs for portfolio trades. According to the UPIA, the trustee is responsible to make sure that the fees charged are reasonable and within current industry standards.

Establishing the Scope of Delegation

A trustee who is working with an investment advisor should institute a specific process. Part of this process may involve questionnaires or supporting documentation related to the trust or trust beneficiary. This documentation plays a critical role in the trust’s investment process and can be used as evidence of delegation. Some of the information that may be provided to the advisor could be:

- The account title. This can help the advisor determine the type of trust that needs to be managed. The title on the account will also indicate who has authority to act as trustee.

- Contact information for those who will act as trustee.

- The date of the trust, most recent amendments, or court appointment dates for court supervised trusts.

- Income/expenses and whether the income and expenses are inflating or non-inflating.

- Age of the beneficiaries to determine life expectancy time frames.

- Mental and physical health status of the beneficiaries.

- Copies of investment statements with accurate tax basis of the assets included.

- Copy of most recent tax return.

As part of the delegation process, the investment advisor should create an Investment Policy Statement based on the information provided.

Investment Policy Statement

An Investment Policy Statement (IPS) is a written document drafted by either the advisor, the fiduciary, or the two together. Based on the trust information and trust beneficiary information provided by the trustee, the IPS should provide general investment goals and objectives for the account. The statement may outline the general rules for the manager to follow in managing the portfolio. The document is usually a written agreement between the fiduciary and the investment advisor.

Investment Recommendation

Within the IPS should be an Investment Recommendation (IR). The recommendation should be specific in providing investment objectives and a suitable benchmark with which to measure performance. It also may describe strategies the investment advisor may employ to meet these objectives. Specific information on asset allocation procedures, diversification, risk management, returns expectations, and liquidity requirements may also be included.

These investment strategies and objectives should be made with UPIA compliance in mind. The IR should address whether the portfolio will be managed or unmanaged and whether the investment advisor will have management discretion. By carefully choosing the advisor and giving management discretion, the trustee is able to start transferring potential liability for management of the assets to the advisor.

Monitoring and Reviewing the Agent's Performance and Compliance

Liability is not transferred, however, if the trustee does not monitor and review the investment advisor’s performance. If the trustee has delegated management, the investment recommendation should also provide the required reporting parameters agreed upon between the trustee and advisor. These reporting requirements should be related to the UPIA’s requirement for risk, return, and diversification. The requirements should also specify the frequency of the reports and the period of time used for review.

As trustees review the trust’s investment returns, risk, and its compliance with the UPIA, they should review it in light of Section 8 of the UPIA which states:

“Compliance with the prudent investor rule is determined in light of the facts and circumstances existing at the time of a trustee’s decision or action, and not by hindsight.”

Certainly not all investment decisions will be successful, but it is important that a trustee show evidence of monitoring the advisor. Ongoing monitoring is also a way to provide evidence that the advisor sought to comply with the UPIA throughout the investment management process. If the monitoring determines that the trust is off course and not meeting the objectives, the fiduciary should request corrective measures lest they risk the chance of being held liable for mismanagement due to neglect. The ability to delegate investment authority provides a way for a trustee, who might not have the necessary expertise, to still stay compliant with the UPIA. But it does require a continual collaboration between the trustee and investment advisor. Done properly, trustees are able to displace their investment liability to the financial professional.